When businesses and marketers think about customers, the focus is often on immediate transactions: what people are buying now and how. Marketing strategies, then, involve valuing these customers only over the short term.

However, when it comes to driving profitable growth in the long term, customer lifetime value (CLV) is a metric that can no longer be ignored. CLV, which measures the total value a business receives from a single customer over their entire relationship, is an ideal way to acquire, develop, and retain the most valuable customers for business growth.

Companies can benefit from having a clearer understanding of how to invest in long-term customer relationships instead of optimizing volumes of short-term transactions.

However, the simplicity of CLV — a single metric that quantifies the future value of each customer — can mask the challenges of implementing it.

Here are five tips for companies as they start their journey to adopting CLV in their own businesses.

1. Look as far ahead as possible

Despite the well-established history of CLV models, shifting from short-term to long-term thinking, especially with a predictive metric, involves the perception of risk. What if the model is wrong? What if my customers behave differently from any other business? The discount factor — finding future cash flow values — in the CLV model includes some level of risk and uncertainty. To help moderate these risks, companies will often truncate their calculation of CLV to fit their existing short-term mindset of six- or 12-month projections.

Avoid this temptation. Narrowing your understanding of the future could deprive your business of valuable opportunities and, just as importantly, valuable customers who may purchase infrequently but spend high amounts when they do so. If your business is stuck, consider running CLV models with both short- and long-term time horizons, focusing on the actual differences between the two. How much value would be given up? What customers or behaviors would be missed in the shorter period? Can your marketing efforts be tailored to acquire the long-haulers while still meeting internal pressures for quicker returns?

2. Don’t drill down too deeply for data

The combination of machine learning and unimaginable amounts of data have led to some companies constructing incredibly detailed behavioral profiles of their best customers: “They exist in this specific market, and they engage with us on this type of device from 3-4 p.m. on Wednesdays.” While impressive, that level of precision may be counterproductive because there are only so many similar customers who may exhibit the same behavior. To borrow from a fishing metaphor, you’ll be more productive with a net than a spear. Keep the size of your prospective audiences in mind as you’re trying to classify user behavior. Start simply by looking broadly for customers who are more valuable than those you are acquiring today, then start to drill down — but not too far.

3. Use the right approach at the right time

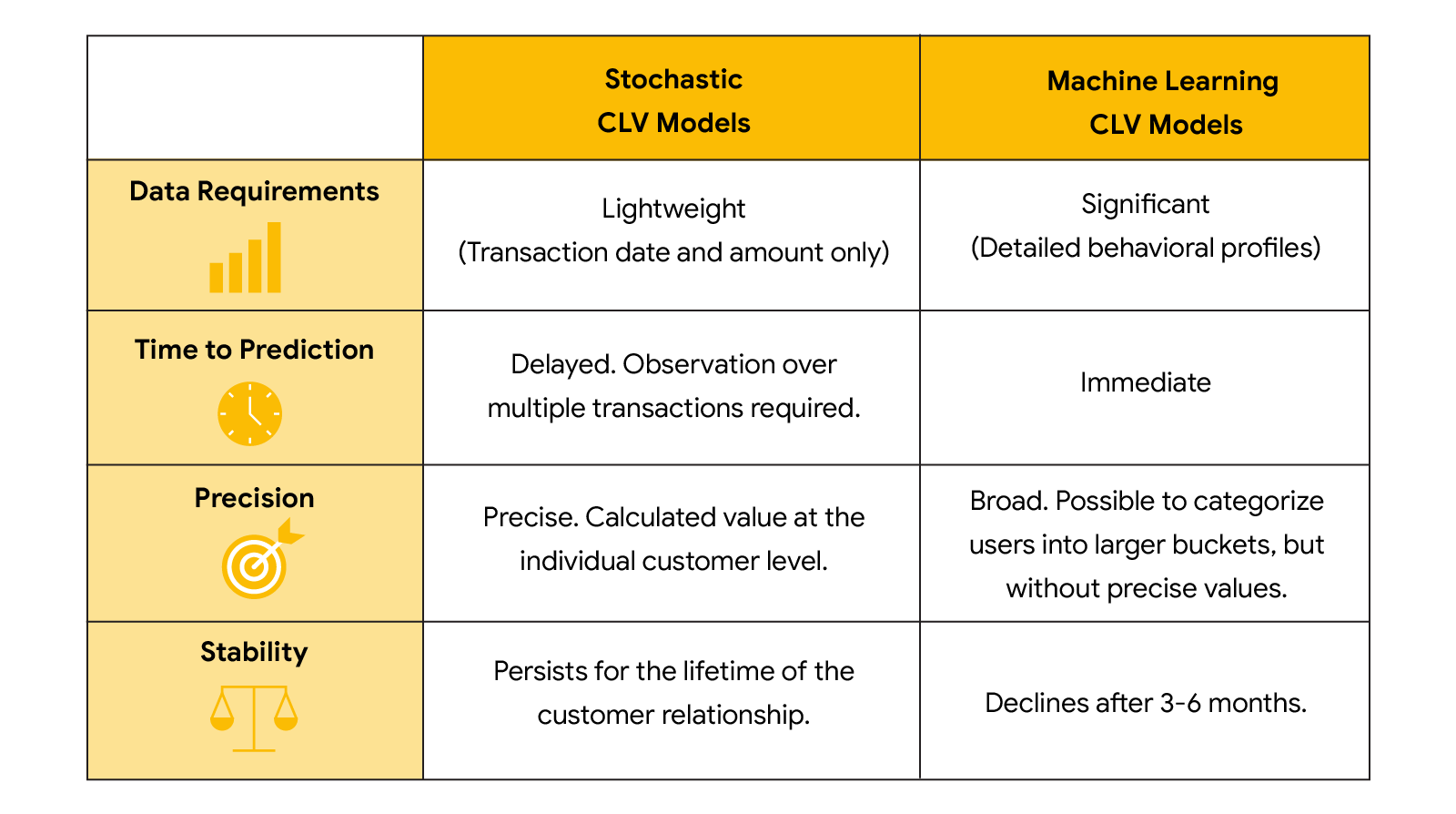

While several types of statistical models, such as negative binomial distribution models, have emerged as favorites for their precision and long-term stability, they require customer observations over multiple periods of time before a prediction can be made. This can make bid optimization for digital ads difficult for platforms that often require a success metric every few days.

Successful advertisers have embraced machine learning as an interim measure for more immediate — although less granular — predictions while reverting to traditional techniques as soon as the customer relationship allows. Be careful to avoid a false sense of confidence, though. It’s necessary to alternate between machine learning and traditional stochastic models, which are random variable models.

Benefits and challenges of different CLV models

4. Always look for new types of customers

The primary source of data for CLV models is your company’s data, but it will be biased because it’s based on the types of customers you’ve tried to acquire in the past. If your marketing actions were oriented toward immediate purchasers, those likely to engage in longer-term relationships may not represent a substantial portion of your dataset. As such, a portion of your marketing budget should always be put aside for exploration — finding and engaging with new types of customers who may be a more substantial source of long-term growth than your current. Put another way, you may not have found your best customers yet. Keep searching.

Put aside a portion of your marketing budget to find and engage with new types of customers for long-term growth.

5. Find ways to appeal to other stakeholders

Adopting CLV can be disruptive: shifting budgets, a delayed understanding of performance, and the gut reaction of judging previous short-term investments in a more critical light. Try to avoid making any large-scale changes at first. Focus on education instead. Help others understand the metric and how it could apply to their business. Be transparent about what will benefit from experimentation, and be open to how they see it impacting their own processes. It may be a slower, more deliberative process, but it improves the likelihood of the approach taking hold.

In the end, perhaps the most important lesson is simply to find ways to integrate CLV into your business rather than shaping your business to accommodate CLV. Be mindful of the guidelines and best practices, but avoid following any metric to such a dogmatic extent that it undermines all the optimizations and processes your business has developed to this point. You were successful because of them, so don’t forget them. Evolve them together instead.