Price, loyalty, and engagement; none of these are new concepts. In fact, they consistently constitute the largest customer challenges in the insurance industry. But change is here and it’s accelerating. In an environment of worldwide economic disruption, increasing regulation, and uncertainty over what will become the ‘new normal’, the insurance industry is seeking solutions to challenges old and new.

U.K. research conducted in late 2019 by market research agencies Old Salt and Little Wing, alongside Google analysis through 2020, reveals how the industry can use technology to adapt to the changing market. We’ve highlighted the most valuable insights to support the case for digital transformation, along with the tools and actions to achieve it.

The evolving insurance customer

Insurance is built on trust, with almost 6 in 10 people saying it’s a key factor when looking for coverage.1 But our research indicates there’s some work to be done here, with 72% consumers seeing insurance as a ‘necessary evil’ — a sentiment that increases with age.2

There are three must-win areas for insurers to win trust: price, loyalty, and engagement.

Price: Understanding the real cost of insurance

For insurers to survive in a highly competitive industry, introductory premiums have become the norm. These discounts can affect profitability, creating false expectations around the real cost of insurance.

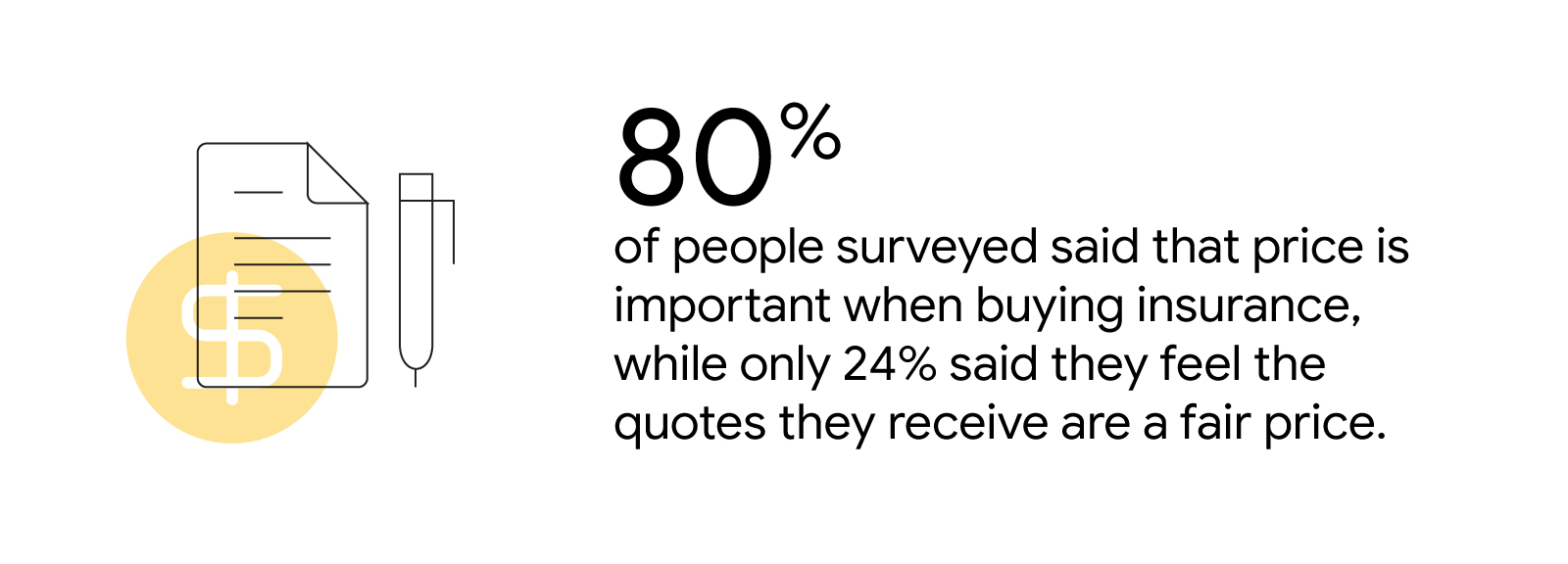

For consumers — often unaware of the changing risk environment — price dominates the conversation, evidenced by the high penetration of price comparison websites. While people have many options to seek out the best deal, what’s clear from our study is that they don’t always feel like they’re getting it. 80% of people surveyed said that price is important when buying insurance, but only 24% said they feel the quotes they receive are fair.3

Search queries in the insurance category often contain price-related terms such as "cheap" or "quote", but it was the modifier “best” that trended throughout the spring lockdown.4 This was particularly noticeable in big-ticket lines such as life and home insurance — where people seemed less concerned about price and more focused on good and trustworthy coverage.

Understanding the basics of coverage also became a theme during this period: “insurance advice” grew by more than 120% year-on-year, while the term “short term” grew 16% year-on-year with consumers seeking out flexibility as working and personal lives changed.5

Loyalty: Consumers feel penalised for being loyal

Our research found a universal desire for consumers to have their loyalty rewarded, yet little understanding of the challenges that insurers face when retaining business. People feel they are being penalised for their loyalty, which creates dissatisfaction and high churn. Of the consumers we surveyed, 41% said they experienced increases in renewal premiums when they believed their circumstances hadn’t changed.6

Google data suggests that people are carrying out extensive research around potential insurers, challenging loyalty: more than 90% of the fluctuations we see in queries for direct insurers can be explained by queries for comparison sites. This implies that in aggregate, users look at both.7 In our survey, consumers reported using two different aggregators during the buying process — comparing deals even across comparison sites.

Engagement: Infrequent customer touchpoints

Improving loyalty and lifetime value can help bring down acquisition costs, but it’s hard to build these when meaningful customer engagement is infrequent. Revealingly, more than 1 in 5 people (22%) surveyed don’t even know who their insurance is with, with this number almost doubling among 18-24s (38%).8

People want their insurance purchase to be quick and easy — and don’t want to think about it again until they need to claim or renew.

We can see this lack of engagement in Google data. The term “check insurance” — which encompasses all the ways people check what their policy covers and who it’s with — has three million searches a year.9 Even outside of the pandemic, these queries remain in the top insurance-based questions asked on search.

3 areas of actions for insurers as consumers become more digital

The data-centric, hyper-personalised approach of digitally focused businesses like ‘insurtechs’ point to some significant opportunities for insurers in overcoming these tensions. Here, we see significant change in not only product but also in business models. We’ve pulled out three learnings — and subsequent actions — that are particularly relevant in these uncertain times.

1. Build loyalty with a holistic, data-driven approach

One in three adults say they’re very interested in having a single policy that covers all their insurance needs.10 For consumers, an all-in-one solution based on their lifestyle helps simplify the admin burden and identify gaps in coverage. For insurers, it allows the opportunity to price more accurately, with more data to understand risk. This leads to economies of scale, which can help reduce premiums and reward loyalty for the number of products held.

Recommended actions:

- Establish the right foundations. Legacy systems and siloed databases by product are long-standing challenges. Audit where your customer data sits across your organisation. Work with those teams to build a case to break down silos and create common data warehouses.

- Power the decisions that matter. First-party data is increasingly becoming a competitive advantage in a cookieless, privacy-first world. Engage with your tech and marketing partners to understand how to leverage an integrated view of your customer across business operations such as planning, activation, and measurement.

2. Explore automation for a more seamless customer service experience

In our research, consumers expressed a desire for convenient, seamless experiences, without, for example, the need to update their insurer of changes to their circumstances — something machine learning can facilitate.

Recommended actions:

- Automate for dynamic coverage. Consider automating cover to a consumer’s precise circumstances, such as by-the-mile car insurance where prices are set according to when and how a car is used. This is beneficial, for example, during periods of lockdown where cover can be automatically paused or reduced to reflect changes in mobility.

- Build quality customer engagement through every touchpoint. Engagement means different things to consumers along their insurance journey. With 56% of insurance queries done on mobile,11 making sure you are ready to meet consumer needs with a seamless experience across devices is a great first step. Cloud solutions such as Contact Center AI can also help automate parts of servicing or claims, especially when call centre capacity fluctuates, such as during the lockdown.

3. Adapt to changing customer needs by being more granular

There’s been a surge in demand for niche coverage such as wedding insurance and working-from-home insurance this year. With fewer like-for-like products in these spaces, consumers are more inclined to focus on features over price.

Recommended actions:

- Highlight benefits that serve specialist audiences. Providing bespoke coverage for specialist activities can more easily avoid the “race to the bottom” so often seen with mass-market products. In addition, those who clearly delineate pricing may also build brand value and inspire loyalty.

- Identify high-quality, targeted commercial propositions. We saw significant disruption in consumer behaviour during the pandemic. Ensure you have your finger on the pulse of fast-moving trends to reach the right customers with the right message at the right time. Google or first-party data can be leveraged to identify niche audiences based on interests or life stages and move quickly to market.

The tensions of price, loyalty, and engagement are as old as the insurance market itself. And in this challenging environment, the only certainty is change. However, by meeting the demands of more digitally focused consumers to become more holistic, automated, and granular, providers can build the agility and resilience needed to meet changing consumer needs and comprehensively insure in the future.