January may be when people set their New Year’s resolutions and hit the gym, but March and April are when people decide to get fiscally fit. These months are the most popular time of the year to open financial investment accounts.

When I opened my first investment account, I went to a physical location and sat down with an adviser to talk about my options. But that’s not the way people are shopping today. The way people are discovering information and narrowing down their options has fundamentally changed. In this Age of Assistance, people expect their shopping experiences to be frictionless, personal, and helpful.

We wanted to dig into how people are shopping for financial investment products and services, so we partnered with the Boston Consulting Group. Our key takeaway? Wealth management customers at all levels rely heavily on digital to help them make decisions at every step of their journey—even if they don’t sign up for an account online.

Researching early and often

Today, people look to their phones for almost everything—from booking a restaurant to browsing for a new jacket, to learning about their digital banking options. They are looking for ideas and advice, researching every decision they make—no matter how small.

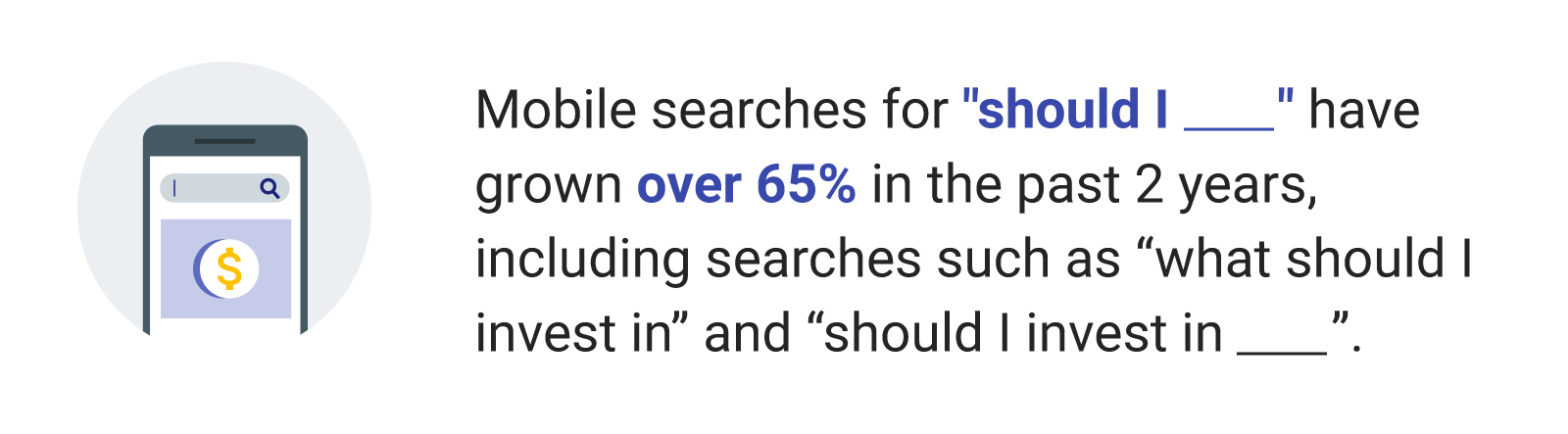

For example, mobile searches with the qualifier "should I ______" have grown over 65% in the past two years, including searches such as “what should I invest in” and “should I invest in ___”.1

When we dug into the research, we were surprised to see that people are turning to digital very early in the research process. Many people are using it as a tool for learning which products and services are available. In fact, over half of online investors don’t even have a brand in mind when they start looking.2 That drives a rigorous online search process, with 86% of potential investors spending more than an hour researching online.3

Still, some people want to seal the deal offline. One out of four investors prefer to open an account in-person, over the phone, or in a branch.4 But those offline investors are still heavily influenced by digital—more than half gathered information online first. They’re checking out specifics products or services, contacting customer service, and scheduling appointments at a branch.

Meeting consumer expectations will define growth

As technology advances and shopping behaviors continue to evolve, a brand’s ability to meet consumer needs and expectations will define its capacity for growth. For financial services brands, this means embracing the fluidity between online and offline shopping behaviors and developing marketing strategies accordingly.

There are big opportunities for brands that act. We’re already seeing financial services brands shift their strategies to account for these new consumer behaviors. They are working on realigning attribution to take into account all touchpoints and conversion channels. They’re pushing to create a systematic test-and-learn roadmap that can inform pre- and post-campaign analysis over time. And they’re enabling cross-channel collaboration and measurement by breaking down organizational silos.

Accounting for these shifting consumer behaviors will require some big changes. But with big changes come big opportunities.