A year after Singapore’s central bank opened up applications for digital banking licenses to nonbank businesses, the Monetary Authority of Singapore (MAS) announced four successful digital bank applicants, including a consortium between Grab Holdings and Singtel for a Digital Full Bank license and Ant Group for a Digital Wholesale Bank license.

The central banks of Malaysia, Thailand, and Vietnam have also been drafting their regulatory frameworks, marking the first major change to the region’s consumer banking sector.

These developments mark a great shift in the banking experience. Here, we look at the digital financial services opportunities brought on by these changes, how banks should rethink their finance apps, and how financial services marketers can pivot their strategy to prepare their business for the future.

Digital financial services have been in the spotlight in recent years. Shifting banking capabilities from the web to apps has played a big role in driving digital financial service adoption.

AppsFlyer released a report in April 2020 that tracked 4.6 billion app installs from 2017 to 2019 across more than 3,000 apps globally, in Indonesia, the Philippines, Malaysia, and Vietnam. The data showed that finance apps have one of the highest growth rates — forming 4.5% of all apps installed globally and almost doubling (+87%) in the past year.

COVID-19 has accelerated this growth. As countries battled the pandemic’s first wave earlier this year, we saw significant increases in worldwide app usage, with a 40% year-over-year increase in Q2 2020 and 25% in Q3 2020.1

Leading the pack: SEA dominates in the financial services apps arena

Southeast Asia (SEA) has one of the fastest-growing digital and mobile-first populations globally — where people use their mobile phones for a variety of activities, including their financial needs. The digital financial services (DFS) market is poised to hit $786 billion in 2021, growing at 14% year-on-year to 2025. Indonesia, the Philippines, Vietnam, and Malaysia ranked among the top 15 markets globally for the number of finance apps downloaded. Of these, loan-related apps made up around half the downloads, whereas investment apps made up an additional 25%.2

The COVID-19 effect was also very pronounced in SEA. It brought about permanent and massive growth in digital adoption as users tried new digital services for the first time. In fact, one in three digital service consumers were new users of a particular service in 20203 and will continue using such digital services. Additionally, 94% of new users intend to continue with app-based services post-pandemic,4 and existing users are also spending more time online each day exploring digital services — an increase of an hour, from 3.7 to 4.7 hours each day.5

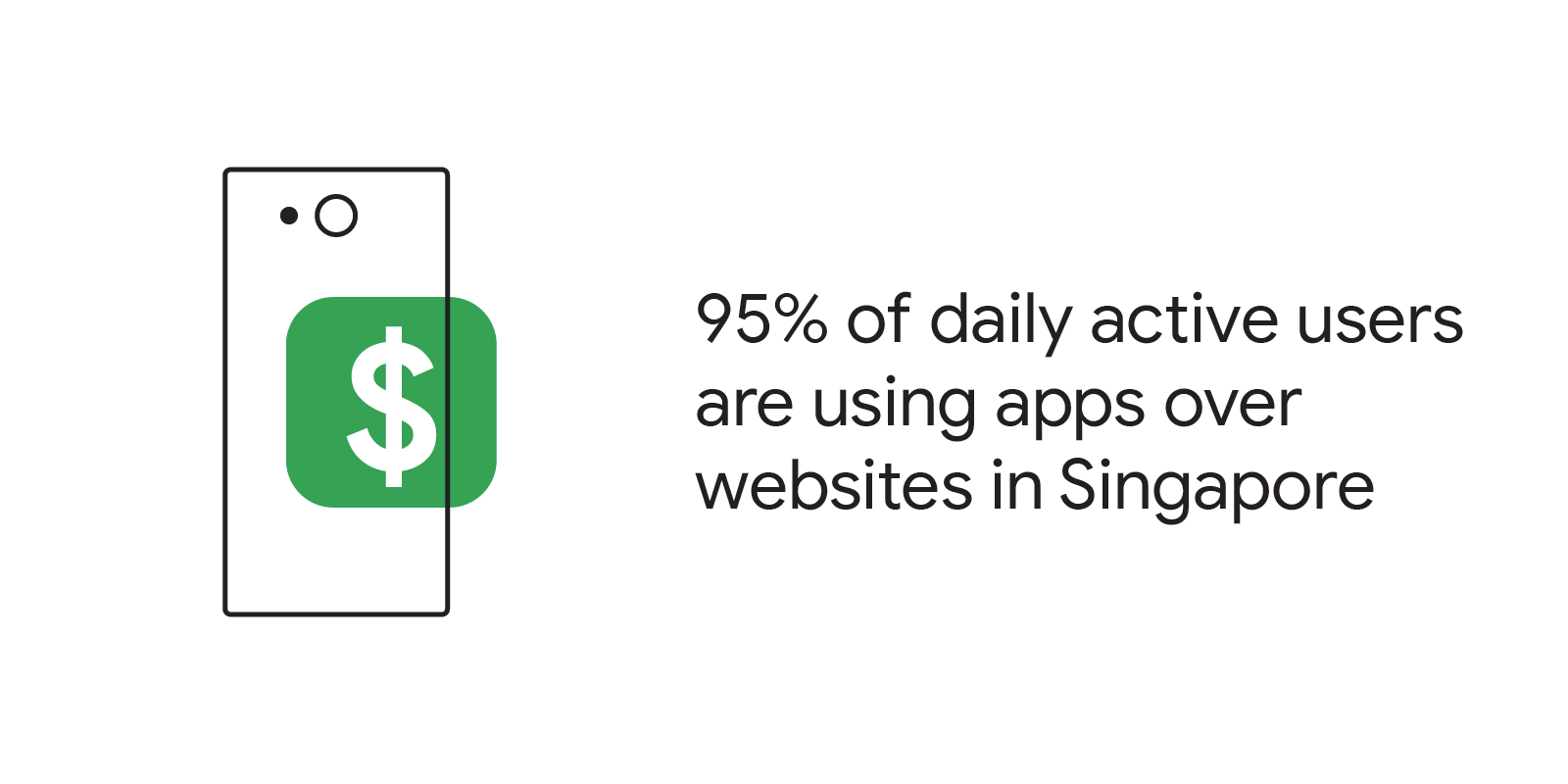

In Singapore, the DFS market is projected to be $130 billion in 2021 — the second biggest after Indonesia — with an average compound annual growth rate (CAGR) of 8% until 2025.6 Finance is one of the most app-driven industry verticals, where daily active users increased by 40% in just two months. At the same time, more than 95% of daily active users are using finance apps over websites, even when compared to e-commerce providers such as Amazon Singapore, which sees around 85% of daily active users on their app compared to their website.7

This trend is accelerating further. For example, finance app adoption grew in Singapore by 16% during COVID-19, with an 8% drop in web users over the same period.8 We are expecting to see a similar trend across SEA.

Since MAS awarded digital licenses, consumer interest in digital banking has been piqued: Google Trends indicates that there has been a 4x growth in search demand on the term “virtual bank” in the last seven days.9

In this new age of banking, with consumers moving toward apps for financial services, both new digital banking license winners and incumbent banks will need to ensure they focus on their app strategy for better customer engagement and acquisition.

Banks like DBS and TMRW by UOB have been key players in the region, pushing ahead with digital financial services that go beyond payments and simple transactions.

However, the profiles of new players are different. These are digital-native consumer technology platforms, spanning e-commerce, ride-hailing, and food delivery, and competition will become much stiffer in the battle for customers’ wallet share. These new entrants have large user bases and high-frequency touchpoints, making their apps very sticky. They are also extremely data-rich, with more information about customer habits and demands than banks — which is an immense advantage. Incumbent banks will need to continue to adapt their strategy.

Acquire and engage: Drive business goals by matching customer demand

Although apps are primarily used for checking balances, paying bills, and peer-to-peer (P2P) transfers, search interest shows that users are now looking for more varied financial services.

In 2020, payment-related queries saw a 50% increase in search interest, whereas search queries for investment services, including online brokerages and forex trading, saw an exponential increase of more than 90%, year over year — outpacing search interest in more traditional and transactional financial products such as credit cards and personal loans.10 In particular, we see increased interest in investments and wealth management apps — a category that is valued at $17 billion and growing at 28% CAGR until 2025.11

This trend is consistent across branded and generic search queries, as well as app queries in the Play Store.12 This is a strong indication that consumers are open to using app platforms to acquire financial products and services beyond simple transactions.

Existing banks are starting to explore new ways to acquire customers — such as encouraging them to invest or apply for new credit cards through their apps. However, there is a lot more room to be innovative here. Apps can be a revenue-generating asset that offer products that are similar to those available on web platforms or at physical branches.

New digital banking players are already gearing up to offer these services. Earlier this year, Grab acquired Bento, a wealth solutions service, which will be rolled out across SEA, with Singapore as its first market.

Taking action: What this means for the banking sector

These trends bode well for winners of Singapore’s digital bank licenses, who are likely equipped to be app-first. However, this also implies that existing banks need to develop and implement a strategy that utilizes their app as a primary customer acquisition and engagement platform to adjust to changes in the financial services ecosystem.

1. Think big but start small with your app strategy

- Focus on bridging the gap between business and marketing objectives that will enable your app to be the central platform for customers to access your services, purchase products, and engage with you.

- Bring product, technology, and marketing teams together to build an end-to-end vision for your app and make it central to your digital acquisition and engagement strategy.

- Most importantly, don’t wait until you have every piece in place because momentum and speed are critical elements. Start with small experiments to test what works best for your target audience and your business, using the findings as a foundation for future iterations.

Tip: Consider driving the specific app action you want when first acquiring consumers, rather than after downloads — this could be a payment service or credit card sign-ups. App Campaigns’ machine learning can help optimize for and target new and existing consumers to enhance app engagement, increasing not only quality downloads but post-download app usage as well.

2. Plan with an app-first approach to acquire and engage with customers

Although app usage is increasing, only 40–50% of people who install an app continue to use it regularly, despite active efforts by banks to engage their customers organically — for example, through in-app notifications or email.13 This existing user base is a missed growth opportunity. To reach out to the dormant half of the base, a targeted approach would be more effective than the usual organic channels.

Tip: An easy way to increase engagement among existing users is by testing with app campaigns for engagement for a consolidated and targeted way to reach app users across Google channels and increase the likelihood of higher conversion rates.

For instance, app-first Russian bank, Tinkoff, relied heavily on video and app store platforms in its marketing mix to engage customers — especially in cross-selling noncomplex financial products like credit cards. According to The Banker’s Top 1000 World Banks 2019 ranking by capital, Tinkoff Bank topped the list of the most profitable banks in Central and Eastern Europe.

3. Improve your analytics by measuring end-to-end app engagement

Most banks are already using analytics to understand their customers’ in-app behavior and interests, but often this is limited to trends and insights such as how often they log in to check their balance or the most frequently used in-app services.

But analytics can also be used to track and evaluate return on investment (ROI), such as revenue, conversions, or sign-ups per dollar spent.

E-commerce players have made a deliberate effort to measure end-to-end user journeys from Search through to in-app product purchases. For example, if you searched for a pair of wireless headphones on Google, the results would direct you to product links within the Shopee app for ease of purchase — this makes it easy to measure a consumer journey.

Marketers and analytics departments are aware of the value in measuring ROI and tracking profitability; however, they face roadblocks from legacy technology limitations, as well as compliance or data privacy concerns.

Tip: Create a sandbox environment that incorporates end-to-end tagging (from spend to conversion) to test the impact of incremental spend and ROI objectives, such as the number of people who sign up for a new trading account.